According to Kiplinger, "The biggest threat to retirement wealth is withdrawing too much money from a shrinking nest egg, because there may not be enough left to benefit from the inevitable market rebound."

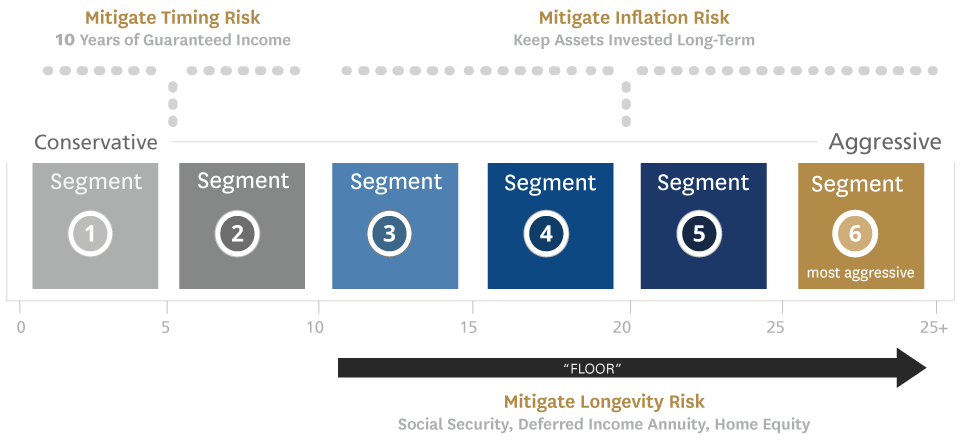

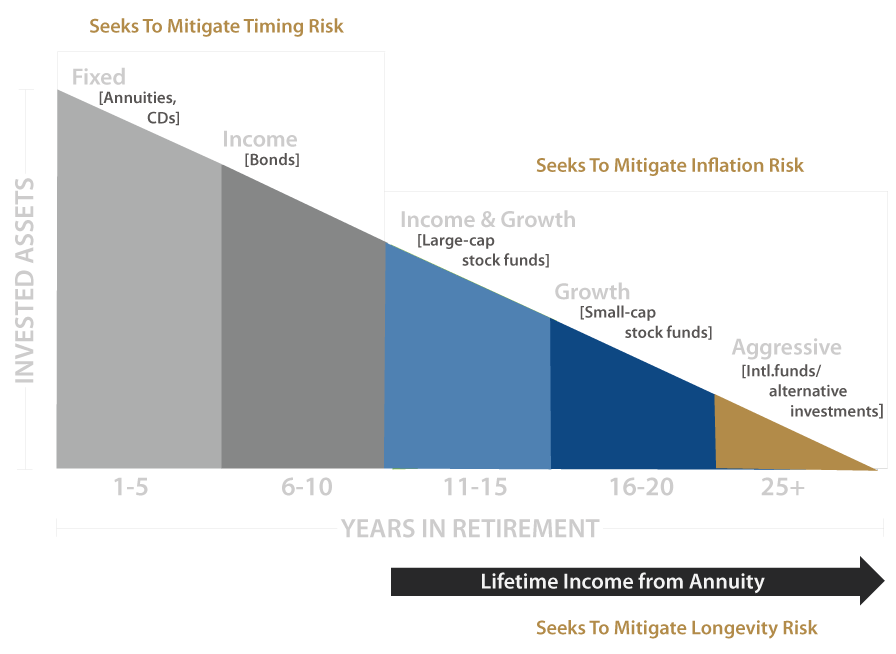

That statement is correct, and it argues for "time-segmenting" your retirement savings. Time-segmentation makes it easier to align your retirement timeline with your investment strategy. It may also help you mitigate Timing Risk and Inflation Risk. By supplementing Social Security with a deferred income annuity, you can also better protect against Longevity Risk- the possibility of outliving your income.

In one popular approach your deposit is shown as being allocated to six "segments" that will hold investment assets ranging from very conservative to aggressive. Segment One, the most conservative, receives the largest portion of your deposit - 28%. Successive segments receive, 26%, 20%, 13% 7% and 6% (total 100%). The segments receiving the smallest amount of money are those which hold progressively more aggressive assets. The more aggressive an investment, the more risk it is subject to. These segments will be held for the longest period of time in order to achieve the best possible chance of excellent investing results.

*These percentages will vary based on your NextPhase™ Personalized Analysis.

Retirees who have saved just enough are well-served.

The Personalized Analysis describes your custom plan for creating monthly retirement income.

It shows how your savings can be divided into multiple segments, each one earmarked to produce monthly income during various phases of your retirement: years 1-5, 6-10, 11-15, 16-20 and 21-25. The goal is to increase your income as you age.

Your income plan will include a "Floor", made up of those income sources which are stable and predictable- Social Security, pensions and income from annuities- and an "Upside," which is that portion of your savings exposed to investment risk. In this way, some of your money is exposed to market based growth potential, but your base monthly income is always predictable because it is produced by income sources that are not exposed to market risk. This is the key to a disciplined plan that seeks to keep pace with inflation, and that you can keep consistent with throughout retirement, and through all economic conditions.